The High-Debt Trap — Why Markets Are Sleepwalking Into a Sovereign Crisis

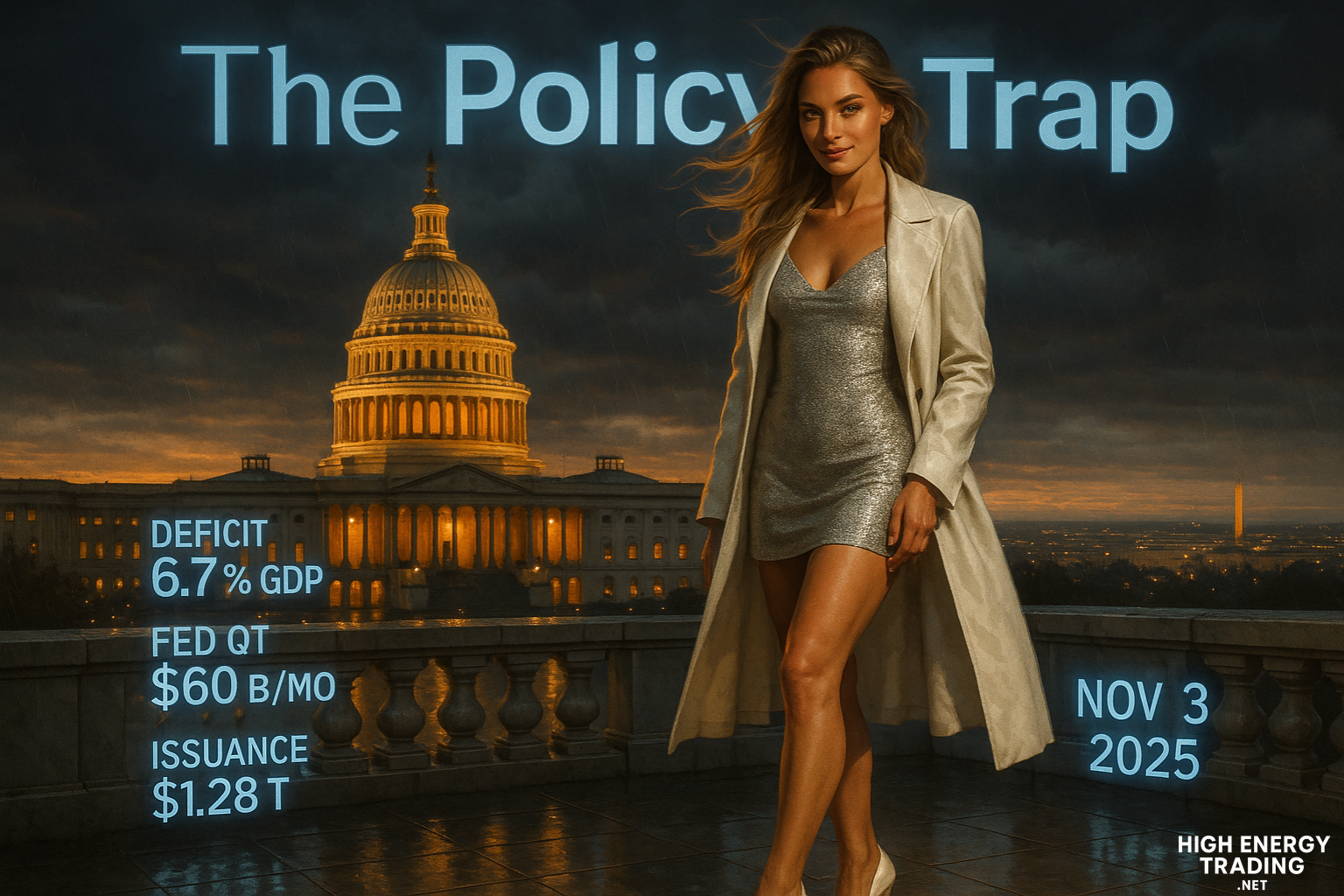

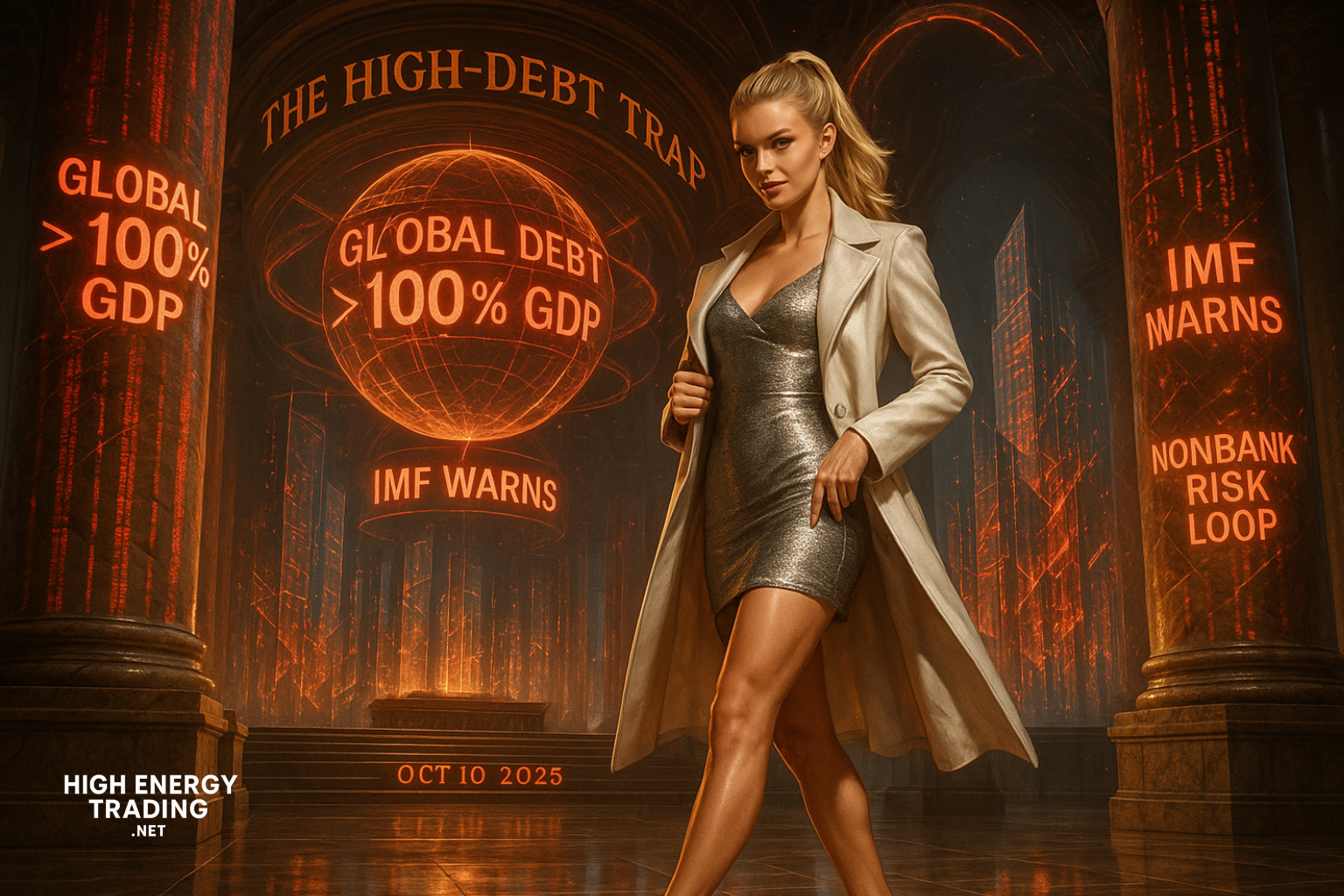

Global debt has just hit a milestone: public borrowing may exceed 100 percent of global GDP by 2029. That is not a theoretical tipping point. It is a condition precedent to stress fractures across rate curves, credit markets, and institutional credibility.¹

Markets are still pricing a “soft stress” scenario. They assume recessions will be shallow, rate moves will be orderly, and sovereign defaults will remain containable. The IMF is pushing back hard: valuations are rich, fiscal tails are lengthening, and nonbank financial institutions are now woven into the sovereign debt nexus as amplifiers, not buffers.²

Here’s what’s lurking beneath the surface — and what could snap first:

Debt isn’t the risk you see — it’s the margin between rates and growth

When sovereign debt surges, the crucial metric is not just debt/GDP. It is **the spread between borrowing costs and nominal growth**. If interest rates exceed growth trajectories for a sustained period, deficits compound reflexively. That is where solvency risk lives.

We already see the strain emerging. Yields on core sovereign bonds are under pressure, while many governments are issuing more across the curve just to roll maturing debt.³ That increases duration risk not just for sovereigns, but for any institution leveraged into bonds.

Nonbank institutions have become the ignition point

Shadow credit — pension funds, leveraged credit vehicles, open-ended funds — now hold significant sovereign debt exposure. In a sell-off, they cannot stop redemptions. They cannot reprice. They become forced sellers. The feedback loop is built in. The IMF warns that interconnectedness and maturity mismatches amplify that risk.²

Sovereign and corporate stress will bleed across borders

Weak sovereigns become credit event candidates. But the contagion won’t stay local. Banks most exposed to frontier or emerging debt will feel it first. Credit spreads in emerging markets already trade near tight extremes relative to macro conditions.¹

Even advanced markets are not immune. Sovereigns like Italy, Spain, or Greece, already haunted by politics, could see funding stress cascade into funding higher costs for corporates, which transmits into credit markets.

What to watch in the next 6 to 12 months

Fiscal revisions: any upward surprises in deficit projections, especially after mid-year budget reviews, should move markets aggressively.

Curve shifts: watch for disproportionate increases in 10s, 20s, or 30s versus 2s and 5s — that signals risk repricing, not optimism.

Credit decompression: widening spreads, especially in “safe” credits, will be the first smoking gun.

Institutional disclosures: look for redemptions, NAV hits, and forced mark-downs in major open-ended funds with sovereign allocations.

Policy surprises: forced issuance, emergency tax hikes, or central bank backstops will turn narratives.

Markets believe the fiscal narrative is under control. They assume central banks will backstop, and debt burdens will remain manageable. The truth is, we are entering a probabilistic era where one shock — energy, war, policy — could blow open multiple balance sheets at once.

What appears as calm today is the first gasp before panic.