The Policy Trap: When Fiscal and Monetary Collide

The U.S. government is now paying yesterday’s promises with tomorrow’s debt.

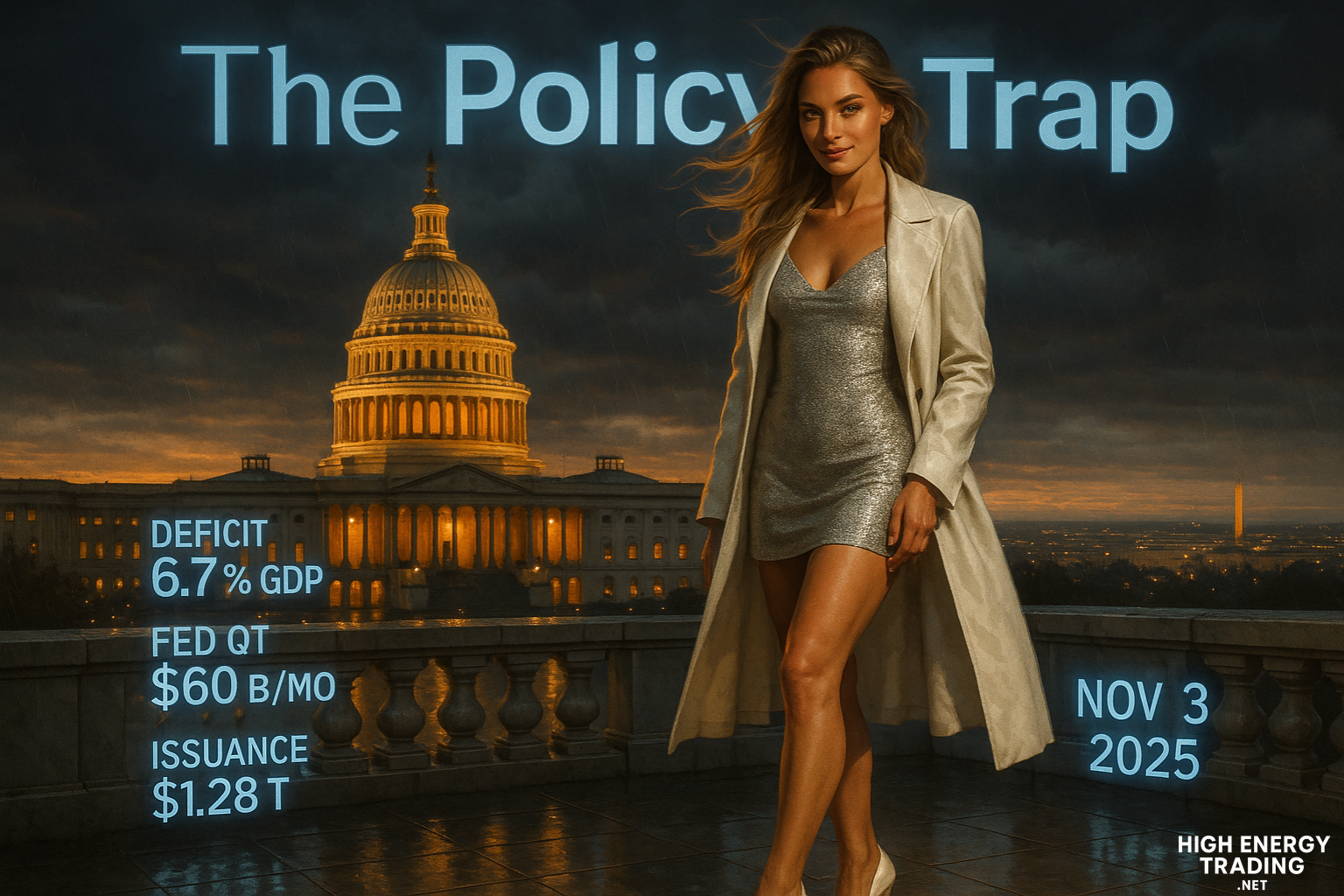

This week’s Treasury refunding announcement confirmed $1.28 trillion in new issuance through early 2026 — one of the largest non-crisis borrowing waves on record. Meanwhile, the Fed continues quantitative tightening, letting roughly $60 billion in Treasuries roll off its books each month. The result is paradoxical: Washington is flooding the market with bonds while its own central bank is draining liquidity.

The trap is self-reinforcing. Each round of issuance lifts yields, which increases interest expense, which expands the deficit, which demands more issuance. Fiscal expansion and monetary restraint are pulling in opposite directions — a feedback loop that markets can no longer ignore.

Investors are starting to call it what it is: fiscal dominance wrapped in denial.

What to Watch

• 10-year yield support at 4.3 % – 4.4 %; a break higher forces repricing across credit.

• Treasury auctions and bid-to-cover ratios — primary dealers’ appetite is fading.

• Fed reverse-repo balances — falling levels confirm liquidity strain.

• Foreign participation in auctions; weaker demand pushes domestic funds to absorb supply.

• Deficit trajectory into an election year — politics and policy can’t coexist peacefully.

Trade Playbook

Long / structural plays:

• Long gold (GLD) as a hedge against policy incoherence.

• Long short-duration Treasuries (SHY) for safety amid yield volatility.

• Long high-quality utilities and staples that thrive in funding stress.

Hedges and tactical trades:

• Short 30-year Treasury futures into heavy auction weeks.

• Long volatility (VIX calls) — policy conflict increases cross-asset swings.

• Short dollar vs gold if deficits accelerate faster than growth.

Alpha setups:

• Monitor T-bill yields relative to SOFR — funding stress appears there first.

• Track Treasury futures open interest; foreign exit shows up before yields spike.